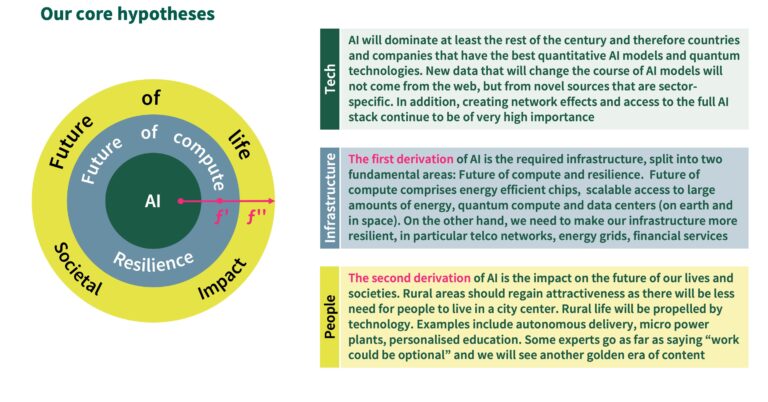

Every era has had a technology that defined its time and reshaped the world as we know it. This is the time of AI – it will dominate for at least the rest of this century, in almost every aspect. The release of ChatGPT was the „Netscape moment“ for AI – not the invention of the new technology, but rather the moment this revolutionary technology became universally accessible. And this has had and will have massive implications with multiple ripple effects. The first derivative of AI is the need to build out the future of compute and the resilience of our energy grids, telecommunications networks and financial services; the second derivative is the broader societal impact of AI and the future of life.

TECH: AI

Within AI, one of the most interesting questions will be how to create a long-term, defensible moat. There seems to be less and less model differentiation as evidenced by API price deflation, rapid benchmarking parity or enterprises focusing on model orchestration rather than model building. However, the real value going forward lies in vertical AI leveraging proprietary data and specialized workflows. Customers want 100% working solutions, not 99%, and the vertical solutions that combine proprietary data + context + workflow on top of frontier models will pull ahead of pure horizontal LLM plays, at least in the professional and enterprise environment. The long-run differentiator becomes the harness around the model, the proprietary data feeding it, the distribution channels reaching the customer, and the depth of workflow integration.

As frontier models converge, the harness (i.e. the orchestration, tools, memory, guardrails, context management, and human-approval logic) becomes the real moat, because it is what turns interchangeable raw intelligence into a reliable, production-grade product. New data that will change the course of AI models will not come from the web, but from novel, sector-specific sources. LQMs (Large Quantitative Models) will be the emerging frontier, with applications for example in molecular modeling, electrical modeling, materials, battery chemistry, drug discovery, and quantitative risk – basically, domains that LLMs trained on internet text cannot meaningfully address.

Creating network effects and access to the full AI stack will continue to be as important as it has been in traditional software. However, foundation models have introduced uncertainty about the terminal value of nearly every traditional software business, which is mechanically expanding discount rates and compressing multiples. Compounding this and in the light of upcoming refinancing needs, the private-equity „floor“ under software has cracked. We will see a re-rating that favours verticalized software with proprietary data and partnerships over horizontal incumbents, unless they are systems of record with network effects.

INFRASTRUCTURE: Future of Compute and Resilience

Future of Compute

AI is the next tectonic platform shift. The transistor led to mainframes, mainframes created the Internet, Internet created desktop, then laptop, and ultimately maturing into today’s mobile and cloud ecosystem. With AI, the innovation cycle compressed from a 10-15 year cycle into months.

Sustaining a position at the frontier of these new platforms depends entirely on access to compute – and the energy that powers it – which remains the single most scarce, yet inevitable enabler for countries and organizations. Hence, identifying and locking in compute capacity is key going forward. In the age of AI, every incremental unit of compute drives innovation, innovation attracts users, and users drive revenue – which is a multiple of the original investment in compute.

Ultimately, in the intelligence age, intelligence is going to converge with compute. The future of compute comprises four main areas: 1) access to energy, 2) energy-efficient chips, 3) quantum computing and 4) data centre infrastructure, including in space.

Electricity is the underlying utility powering compute. Hence, access to near-infinite energy is key. The US-EU-China electricity comparison reinforces the strategic urgency: China now generates 40% more electricity than the US and EU combined with Europe’s terawatt-hours even slightly declining. Electricity output remains the single best proxy for industrial capacity. For the competitiveness of Europe, it will be crucial that companies like Proxima Fusion succeed and can raise the money they need to build at pace and at scale.

Chip development will bifurcate into two phases. In the current phase, gains come from incremental improvement of the existing GPU paradigm, with the next leap in capability driven more by algorithmic efficiency on roughly the same chip-plus-power base. GPUs were never actually designed for AI: the „G“ stands for graphics, and they were built to render pixels in parallel, a workload that happens to overlap usefully with the matrix multiplications behind LLMs.

But language-model computation is not what the silicon was optimized for, and a lot of compute is wasted as a result. A step-function change should arrive within roughly 3 to 5 years, once chip designers start from a clean sheet and ask what architecture they would build if the starting point were brain-like computation rather than legacy graphics hardware. This is the GPU-to-novel-architecture transition. Startups and academics are already working on it, with strong teams not only in the US, China, and Taiwan, but also in Europe and Singapore, particularly in photonics.

This competitive, multi-region race over post-GPU architectures is unfolding alongside another near-term strategic frontier: quantum technology.

Commercialization in the quantum space is bifurcating into two distinct vectors: quantum-inspired classical software and true quantum hardware. Even prior to the deployment of large-scale quantum hardware, „quantum-inspired“ algorithms are gaining significant commercial momentum. By mapping complex quantum mechanics equations onto classical architectures, these models run efficiently on commercially available Nvidia GPUs and specialized accelerators today. This algorithmic approach proves that enterprises do not need to wait for fault-tolerant hardware to leverage quantum physics for advanced optimization and complex data processing. Concurrently, the timeline for true quantum hardware is compressing. Built on qubits that leverage quantum superposition and interference, these machines will compute exponentially faster than classical supercomputers for specific workloads. This unlocks „game-changing“ capabilities in variety of fields requiring immense-scale computations like molecular modelling for drug discovery, material science, and macro-optimization. The urgency of this timeline was underscored in March 2026, when Google announced an internal deadline of December 2029 to complete its enterprise-wide migration to Post-Quantum Crypto-

graphy (PQC). This aggressive timeline to secure global infrastructure against eventual decryption threats proves that the macroeconomic and security implications of quantum are already driving capital allocation today.

Turning to data centre infrastructure, the buildout itself is being redefined. Google announced a joint venture with Blackstone to break the data centre buildout into specialized pieces: Blackstone brings the capital, the physical sites, power procurement, and permitting; Google supplies TPUs, compute infrastructure, and a software stack on top. Ben Trainer, who ran Google‘s entire data centre infrastructure until about a year ago, is leaving to become CEO of the JV. The deal could be a blueprint for various smaller and larger transactions in the space, and it points to where the infrastructure layer is heading next.

The satellite/space market doubled from $300B to $600B over the last decade and is projected to triple to $1.8T over the next ten years. The previous decade used space to enable things on Earth (telecoms, ship/air communications), while the coming decade is about building „space economies.“ Inside that, there are three very interesting areas: 1) in-orbit networks, inter-constellation links, and data centres in space; 2) manufacturing in zero gravity, with pharmaceutical companies exploring drug development in zero-G alongside materials and other goods; and 3) AI and on-orbit processing that happens in space before any decision or transmission back to Earth. Several companies are pursuing each of these today, and they are all real.

The biggest driver of the investment thesis in this area is sovereignty. Each nation wants its own capability to move data through space, partly because terrestrial infrastructure is being targeted in active conflicts. Lunar infrastructure adds a second layer: a return to the Moon will require dedicated communications highways, all routed through space-based assets.

Resilience

The single biggest change reshaping the digital landscape is the rise of AI traffic. A human shopping for e.g. a printer might visit five websites, whereas ChatGPT, Claude, Gemini or Grok will visit a thousand times more of the internet to answer the same query. Non-human Internet traffic will soon rival and exceed human traffic and is growing exponentially. In that context, after years of flattening out, the number of new websites being created has shot back up in the last 18 months because code and content are so much easier to produce.

More sites and more AI agents crawling them fundamentally reshape the attack surface. Every new site is a potential vulnerability, and AI agents introduce new risks through prompt injection, data poisoning, and automated reconnaissance at machine speed.

This is where resilience comes in. Resilience has two sides: enabling resilience, which is about building new capabilities and moving forward, and defensive resilience, which is about absorbing attacks and continuing to operate. Cybersecurity sits squarely on the defensive side. As a matter of principle, bad actors will adopt AI faster than defenders, and every additional layer of digitization widens the gap further. The geopolitical angle compounds this: China‘s coordinated strategy explicitly bundles AI, quantum, and nanotechnology together as the „core digital technologies“ of the 21st-century digital economy. Protecting IP through cybersecurity is therefore essential, so that competitors cannot compress their R&D timelines at the expense of the original.

Within each layer – model, compute, space, security – the pattern is the same: as the raw capability commoditizes, durable advantage migrates to the harness around it, the data feeding it, and the infrastructure under it. That is where the value, and the contest, now sits.

PEOPLE: Future of Life and Societal Impacts

Work

One of the defining questions of the century is what impact AI will have on the future of life, on society, and on (the number of) jobs. Asking people responsible for HR and recruiting what they plan to do with headcount – keep it constant, increase, decrease – one has to concede the question is unresolved. But a general principle is emerging: in any job that bundles a routine, automatable component with a judgment-, trust-, or relationship-based one, AI compresses the routine portion, and the human portion becomes proportionally scarcer, but more valuable per hour. The jobs that genuinely disappear are the ones that were only the automatable task – never really bundled to begin with.

Radiology is a good example. The naive view is simple: a radiologist reads images, so AI can and should replace the role. The contrarian view is that this misunderstands the job because a radiologist‘s real work is actually bundled. Reading the MRI is one task. Explaining the result to an anxious patient and consulting with the referring physician on next steps is another. As AI absorbs the image-reading task, radiologists end up spending more of their day on the patient conversation and the physician hand-off, which is exactly where their training, judgment, and trust matter most. The headcount and pay of radiologists are rising even as headline tasks get automated. Pierre Manceron, co-founder of Raidium, presented his approach to AI and radiology at DLD in January 2026. His point captures the dynamic well: The agent can do the work, but a radiologist must sign off. That signature is the unbundled human part that becomes more valuable the more everything around it gets automated.

The same logic explains why some companies are increasing headcount rather than cutting it: If the human-facing fraction is where the value concentrates, AI-augmented radiologists can handle more cases – and more patient conversations – per week, turning the unbundled portion into the scalable part of the job.

The interesting aspect is that adoption of AI appears to be bimodal: the very junior and the very senior are embracing it, while the cohort stuck in the middle is the 25-to-40-year-olds – older Gen Z and younger millennials. Game-theoretically, they’re rational to resist. They just invested heavily in becoming excellent at the old game, and converting to AI tools erodes their advantage over juniors and interns. Nonetheless, an argument can be made for the fact that it takes deep foundational expertise to safely interpret and audit AI results – expertise juniors may not be able to learn when relying on AI too much.

Education

Building on how the work environment is evolving, it is clear that education and curricula will change rapidly – at both, the high school level and university level – and most likely become far more personalised. As this unfolds, the role of the teacher shifts rather than disappears. When AI absorbs routine tasks like grading, lesson planning, and first-draft feedback, teachers are free to spend more of their time on the things machines cannot do: mentoring, motivation, and social-emotional support. The evidence already points this way, with AI tutoring delivering real learning gains when it is well designed, yet systematic reviews consistently finding that human tutors remain central to effective learning.

Microschools like the Alpha School – using AI for core instructions while humans handle coaching and life skills – are an example of where this could head towards. It will be interesting to observe how universities will adapt and which private players will emerge with alternative offerings. In any case, AI-to-human use must be paired with a human-back-to-AI step – the student reconstructing, explaining, or being tested on the material – or the learning is offloaded rather than acquired, and erodes.

Entertainment

Spotify paid the music industry $10 billion last year, more than the entire industry was worth in 2002. There is an argument that AI could fund a new golden age of content creation and entertainment – but only if the business model rewards real knowledge rather than traffic-chasing. One example is hyper-local, hyperspecific content: exactly what AI companies cannot get elsewhere and are therefore willing to pay for. LLMs are all about words. There is a case to be made that media companies should sell not just the published article but the corpus behind it: for every word in a story there are probably 1,000 words of reporter notes, for every photo about 500 unpublished images, and that depth of data is the real gold mine for any AI buyer. AI companies pay for access to the data they need to close the data gap with incumbents, such as Google – and willingness to pay on those terms is dramatically higher than for ordinary licensing.

But not only AI as such could fuel a new golden era of content creation and entertainment. With substantial efficiency gains in almost every aspect of life, people will have more spare time and will hence look for and consume more content. Areas that will substantially benefit from this are gaming, art and life entertainment.

In-person becomes premium. As AI makes synthetic content abundant and cheap, scarce human experiences (live music, theatre, in-person events) become more valuable. People pay for what is embodied, real, and cannot be replicated and seek togetherness and belonging.

Arts are about to have a huge revolution – human-made and live art stands to command a scarcity premium – not because AI cannot generate images or music, but because AI commoditises mass-produced content while struggling to replicate the authenticated, the embodied, and the emotionally intelligent one.

AI will also fundamentally change the user experience in gaming. Already one of the fastest-growing media categories worldwide, gaming is set to expand further: By 2029, every online adult in the world (3.7 bn) will be a gamer in some form. That ranges from gamified content at the lighter end to fully generative experience games, where players build their own worlds and characters become addressable even outside the game, through chat apps like WhatsApp – until being a gamer becomes nearly universal among online adults.

Rural vs. city life

One of the main reasons people live in cities is the proximity to their workplace. As today‘s technology matures, rural life will regain its appeal, offering a techenabled life in nature. The enablers are stacking up: autonomous delivery, micro power plants, satellite internet, AI-driven medical diagnostics and treatment of routine medical cases, personalised education, and companies built by just one or two people all reduce the need to live in a city, where costs are substantially higher. The case for city life, on the other hand, is the proximity to humans, to shared experiences, and to entertainment.

The privilege of venture capital is thinking about breakthrough technologies that look very unreasonable and unreal at first – until you meet entrepreneurs crazy and driven enough to work on them and make them inevitable. We live in a fascinating time where innovation will happen at an unprecedented pace.